Health Insurance Coverage - How Much?

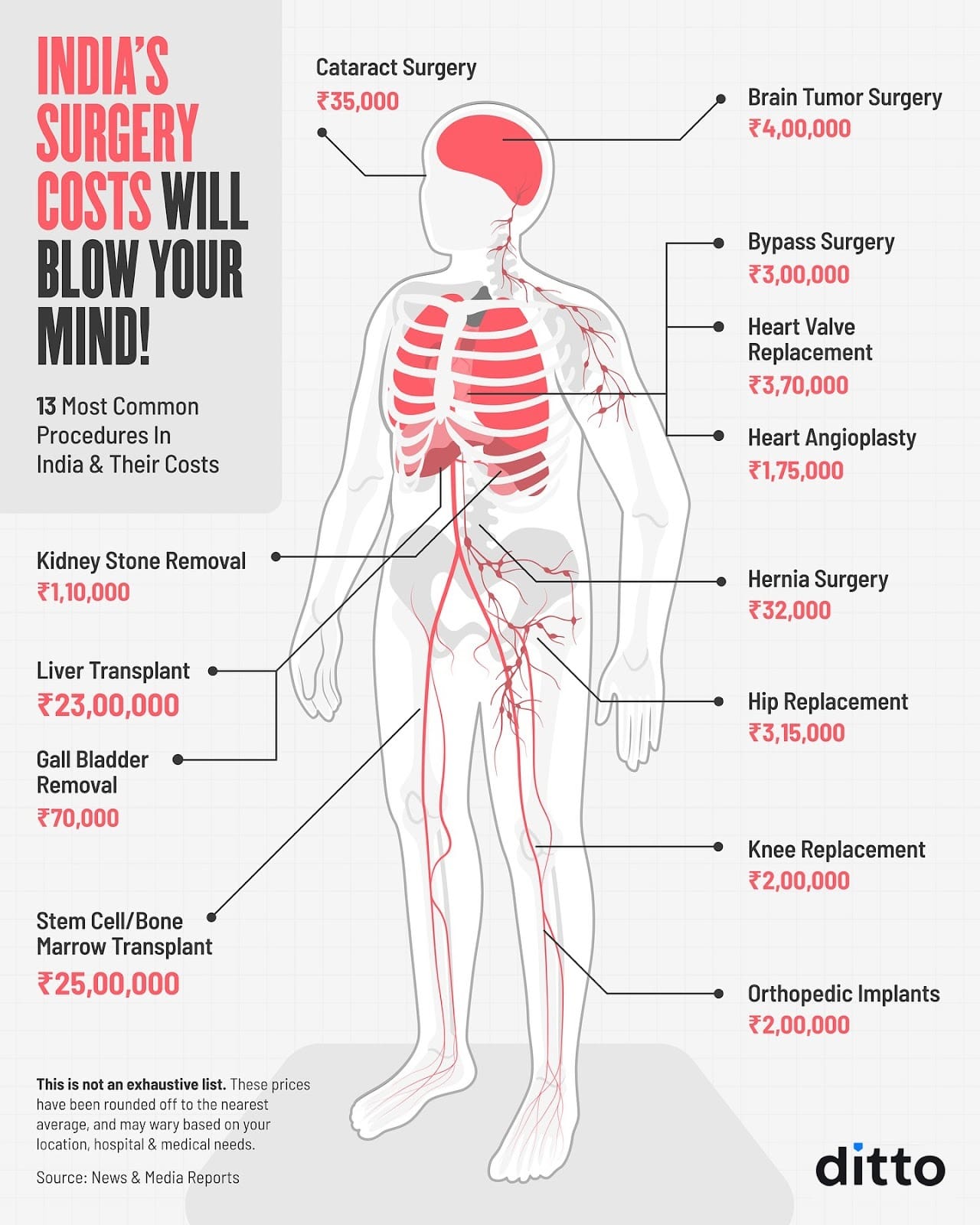

Ritesh Sabharwal CFP®W.M.W #36: Health Insurance Coverage - How Much? Reading time: 5 minutes - February 21, 2026 ↓Hey Reader After publishing my last newsletter, I got several emails mostly asking the same thing: What's the actual health insurance coverage I need? In India, families still pay 39.4% of healthcare costs out of their own pocket.

So what's the right number for you? How Much Health Insurance Coverage Do You Actually Need?Most people go about this the wrong way - they try to predict the exact hospital bill they might face someday, which is nearly impossible. A better approach is to pick a cover that ensures you never have to say, "I had insurance, but still had to arrange a few extra lakhs." The right health insurance cover is simply one that can absorb a significant hospital bill at the kind of facility you'd genuinely choose. For most people, the ideal amount depends on four things below - start at ₹5 lakh and add ₹5 lakh for every "Yes" you answer:

A practical starting point for most people is ₹15-25 lakh in base cover though you might go lower if you're young, healthy, and living in a smaller city. Since medical costs climb quickly, it's worth revisiting your cover whenever your life circumstances change. A few things worth keeping in mind:

To put it more specifically:

One thing worth noting: bumping your cover from ₹10 lakh to ₹20 lakh doesn't double your premium. The increase typically falls in the 20–30% range - a modest step up for a meaningful jump in protection.

If you are seeking clarity for an existing policy or want a new one, book a FREE call --> https://ditto.sh/9q6jpm Key Factors to Consider When Deciding Your Coverage

If you are seeking clarity for an existing policy or want a new one, book a FREE call --> https://ditto.sh/9q6jpm Individual vs. Family Floater: The Real AnswerFamily Floater: One pool shared by all insured members When it makes sense: The risk: If your spouse needs ₹7 lakh surgery and your kid gets dengue for ₹2 lakhs in the same year — your ₹10 lakh floater is exhausted. You're unprotected for the rest of the year. When individual plans make more sense: The practical rule: 👉 Action Steps for This WeekStep 1: Check Your Correct Coverage Need

Step 2: Structure Your Insurance Correctly For most people under 45: ₹5-10L base policy + ₹20-25L super top-up = right structure Step 3: For Parents - Act This Week, Not This Month

The cheapest health insurance policy is always the one that actually pays your claim when you need it.

Got questions about your specific policy or what structure makes sense for your family? Book a FREE call --> https://ditto.sh/9q6jpm Connect with me on LinkedIn, I write every day to help you make smarter money decisions 👇 |

Ritesh Sabharwal

Ritesh Sabharwal CFP® W.M.W #55: Do you know - Your EPF Account Has ₹7 Lakh Life Insurance? Reading time: 5 minutes - July 4, 2026 ↓ Hey Reader Have you heard about EDLI - Employees' Deposit Linked Insurance? Most people reading this right now have this benefit and are not aware. Most haven't told their families about it. Your EPF account comes with ₹7 lakh life insurance. You're paying ₹0 for it and your employer covers the premium.It sits quietly inside your EPF account. It activates...

Ritesh Sabharwal CFP® W.M.W #54: Which is better: 70-20-10 vs 50-30-20? Reading time: 5 minutes - June 27, 2026 ↓ Hey Reader One of the defining financial challenges for Indian households in 2026 is not a lack of income, but a lack of financial visibility and control. Rising living expenses, combined with unprecedented access to consumer credit through EMIs, BNPL platforms, and credit cards, have normalized spending patterns that often outpace financial priorities. Millions of Indians follow...

Ritesh Sabharwal CFP® W.M.W #53: Decode the Home Affordability Formula (3 / 20 / 30 / 40) Reading time: 5 minutes - June 20, 2026 ↓ Hey Reader Reserve Bank of India data shows housing dominates borrowing in India like no other category.Half of India's loans go to one thing: Homes. Home loans: 49%, Everything else combined: 51%. And yet, most Indians are clueless to determine if they can truly afford what they're buying. They walk into a bank. Get told they're "eligible" for X amount of loan....