Miss This Deadline and You May Pay Extra Tax

Ritesh Sabharwal CFP®W.M.W #41: Don't Overpay Taxes: Meet Form 10-IEA Reading time: 5 minutes - March 28, 2026 ↓Hey Reader Open your calendar. Look at July 31 - Something that might ring a bell!! Form 10-IEA. If you have business or professional income and you miss this form, here's what happens: You: "What's Form 10-IEA? Can I file it now?" This exact scenario has played out thousands of times since the government made new tax regime the default from FY 2023-24 (April 2023). The problem: For business/professional income earners, opting for old regime (with deductions like 80C, HRA, home loan interest) requires filing a separate form before ITR deadline. The bigger problem: Nobody tells you this. Not the IT portal. Not the filing software. Not even most CAs until it's too late. Today, I'm showing you exactly what Form 10-IEA is, who needs it, and how to file it in under 10 minutes - before July 31. What is Form 10-IEA?In simple terms: It's the form that lets you choose old tax regime if you have business/professional income. If you don't file Form 10-IEA: You're locked into new regime. No 80C deduction. No HRA. No home loan interest benefit. Nothing. Who Must File Form 10-IEA?You need this form if: You don't need this form if: What counts as business/professional income?Not sure if you have "business/professional income"? You do if any of these apply:

Even ₹1 of freelance income + a salary = you need Form 10-IEA to claim old regime. The Critical Deadline (This is Time-Sensitive!)Form 10-IEA must be filed before your ITR due date. For most people:

Miss this deadline = stuck in new regime for the entire year. How to File Form 10-IEA (Step-by-Step)Time needed: 10 minutes Step 1: Login to Income Tax e-filing portal (https://eportal.incometax.gov.in)

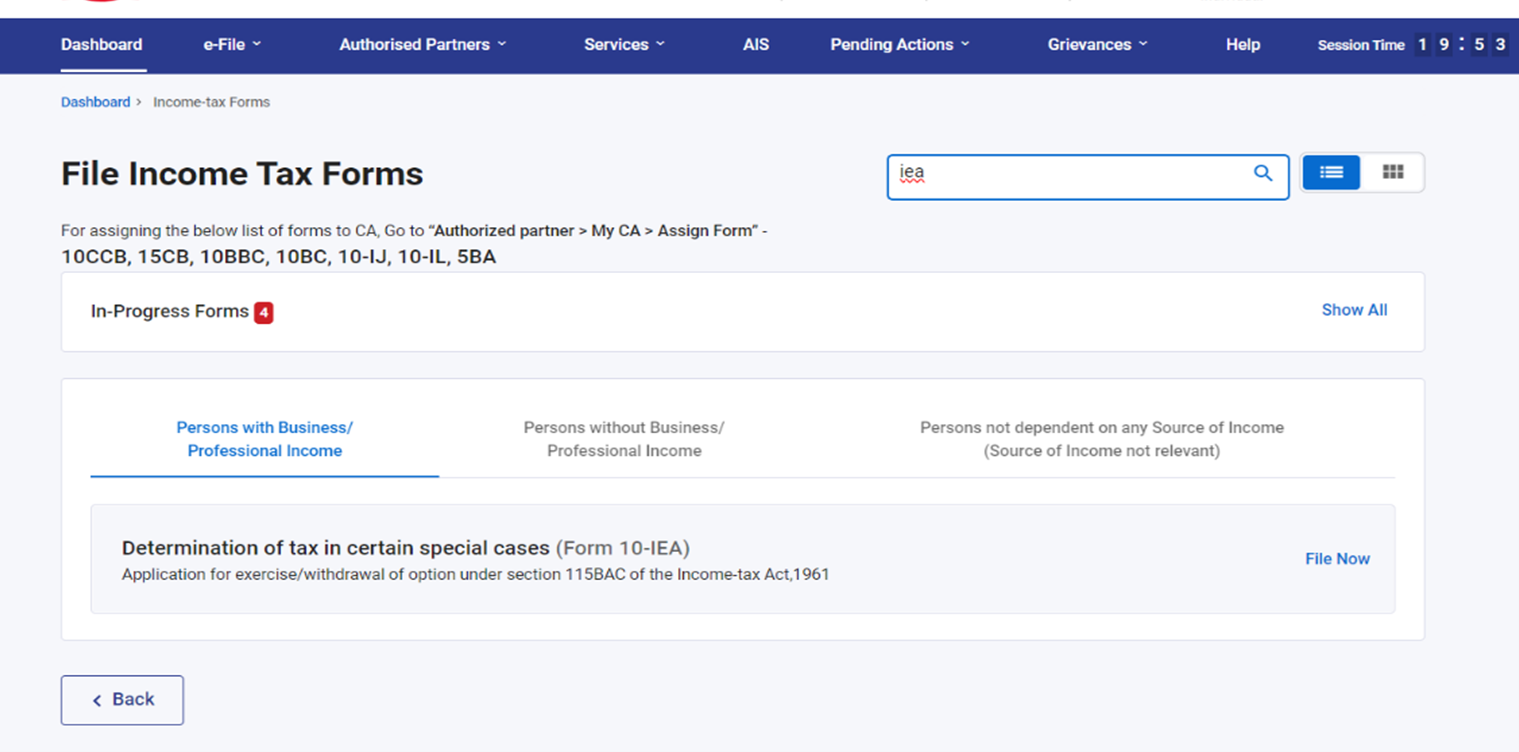

Step 2: Go to e-File > Income Tax Forms > File Income Tax Forms Step 3: Search for "Form 10-IEA" or select it from the list

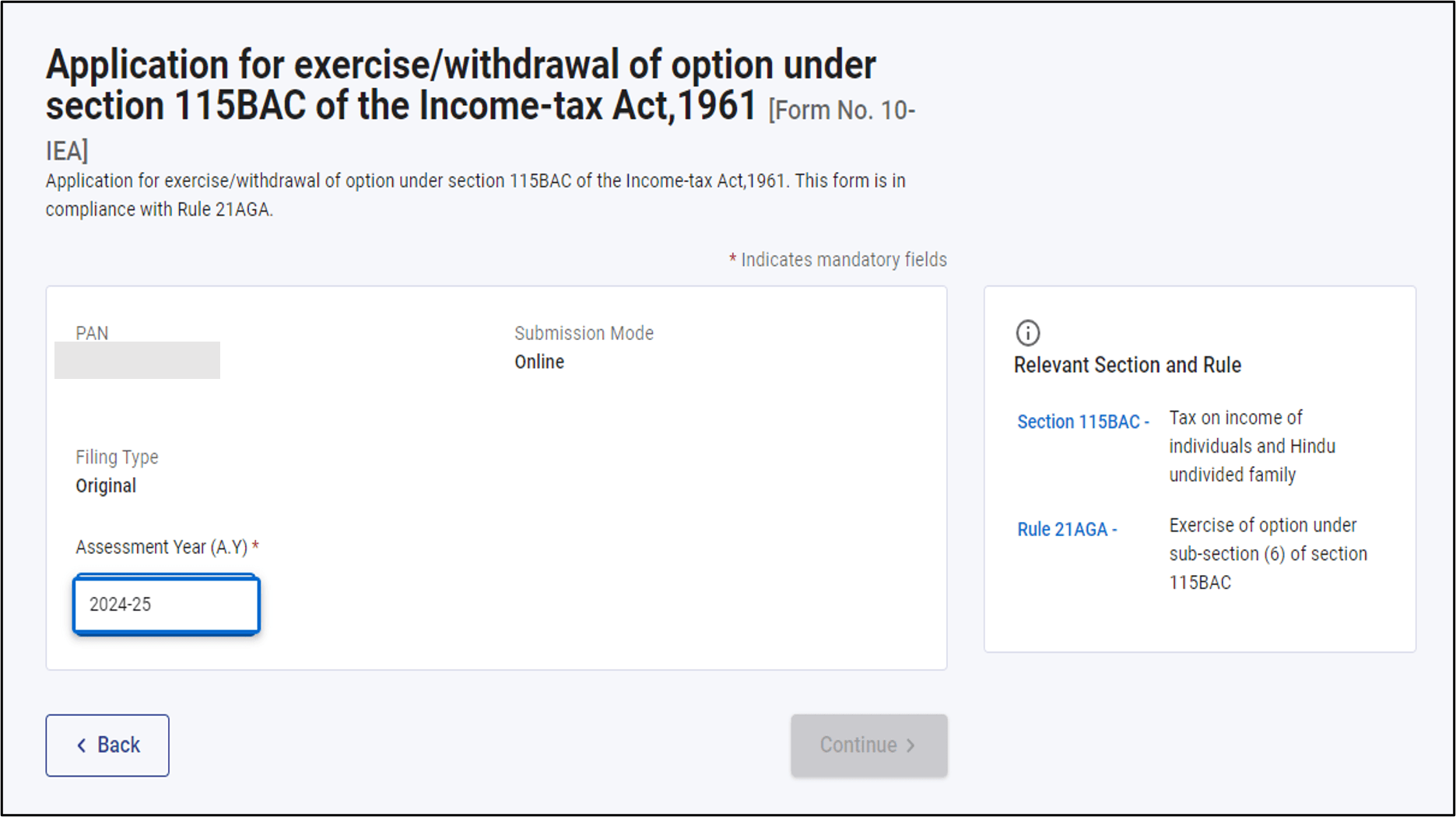

Step 4: Select Assessment Year (e.g., AY 2026-27 for FY 2025-26)

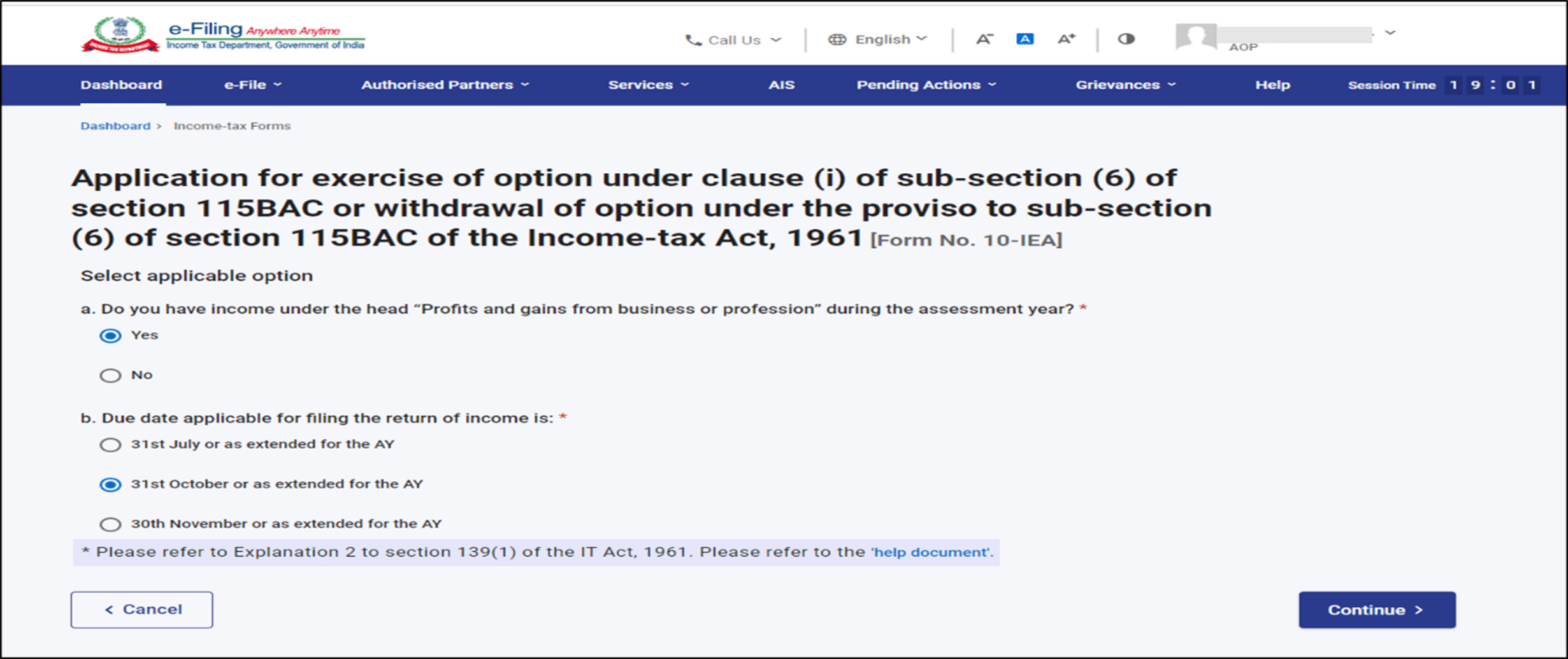

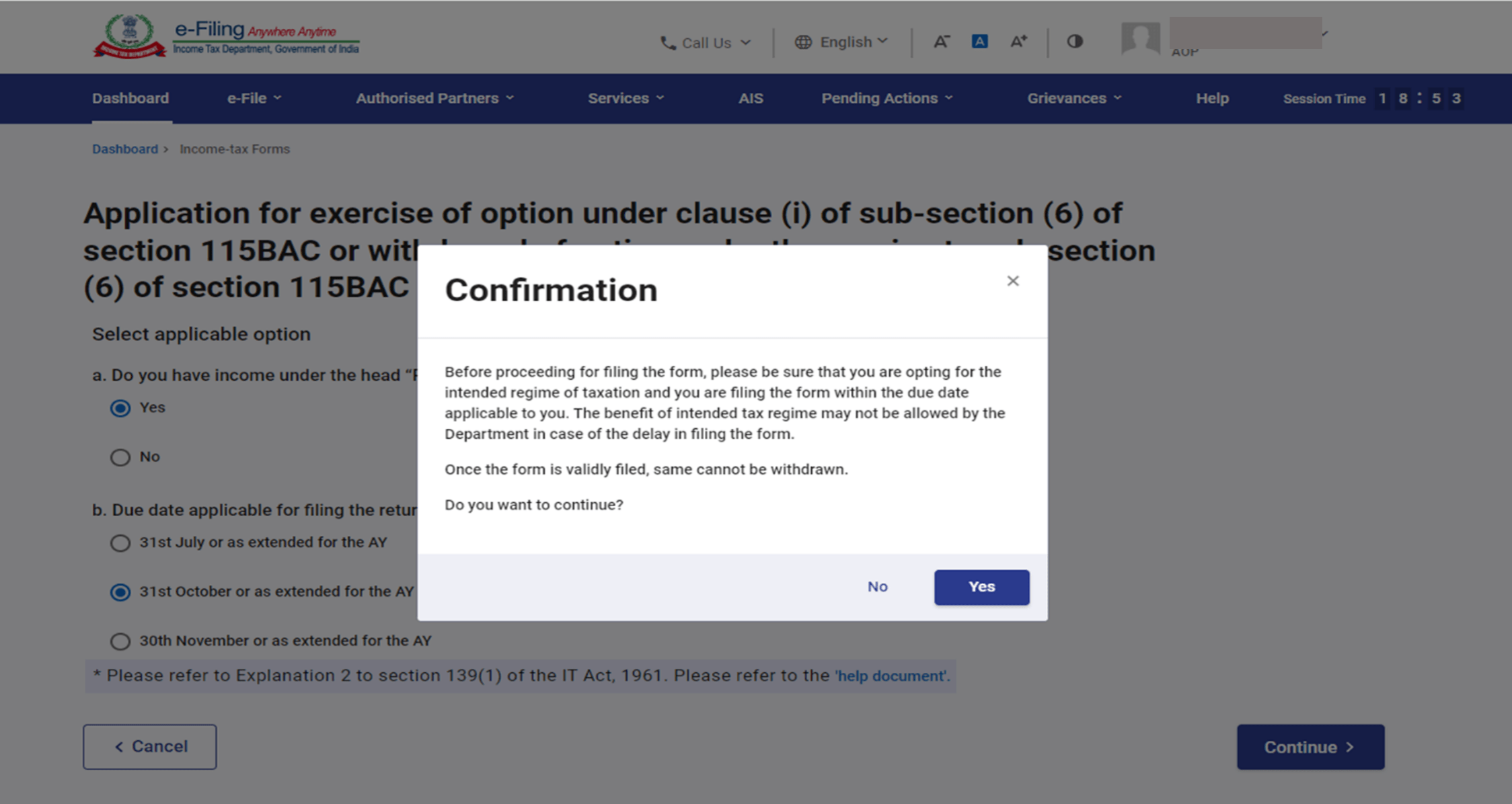

Step 5: Confirm you have business/professional income → Click Yes. Then Select your ITR due date (usually July 31)

Step 7: Confirm selection of Regime

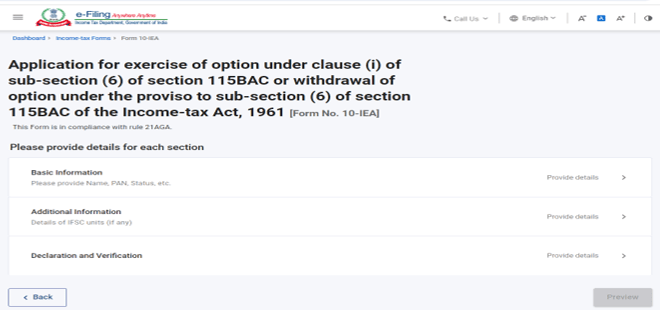

Step 8: Fill basic information (auto-prefilled: Name, PAN, Status)

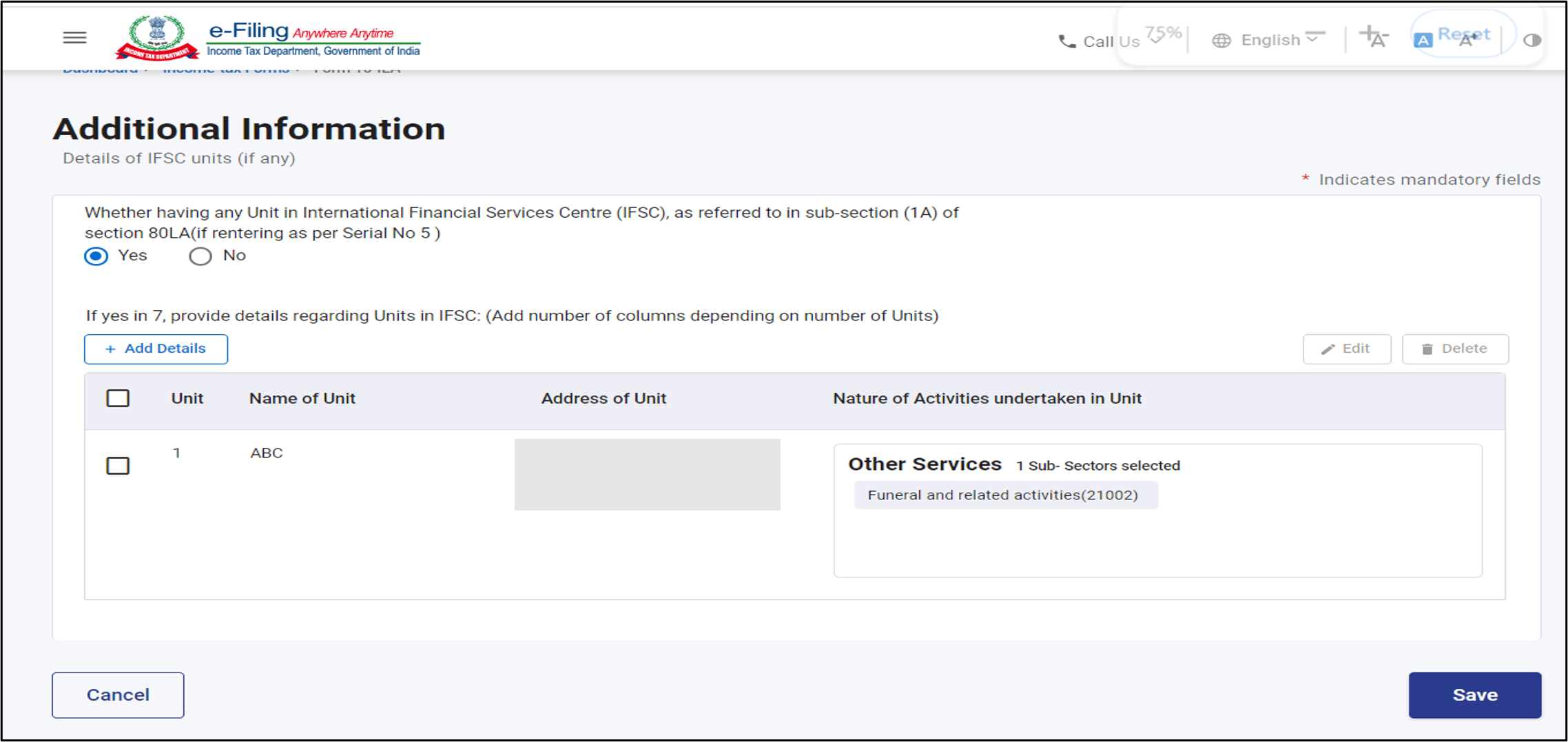

Step 9: Fill additional information (if you're in IFSC unit, otherwise leave blank)

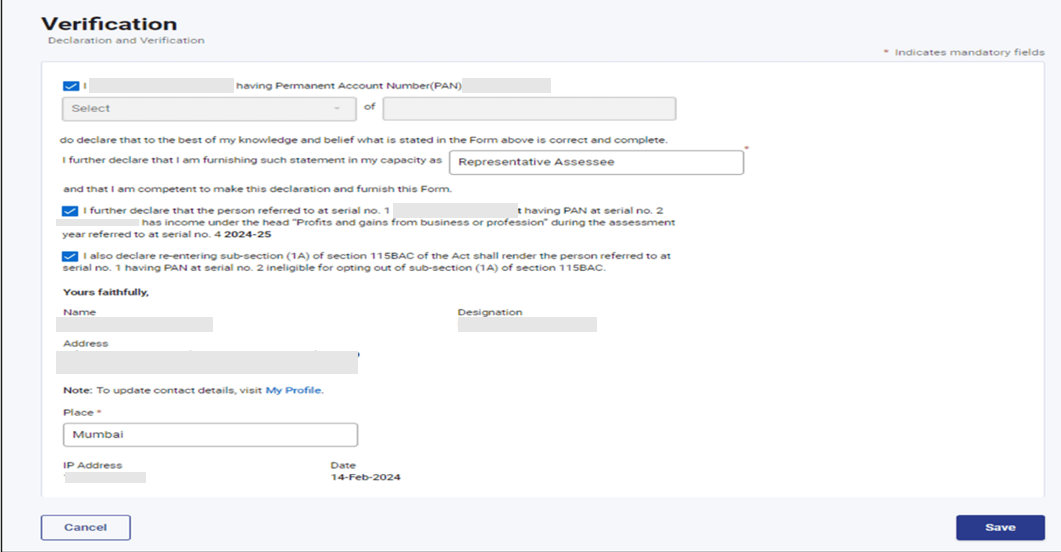

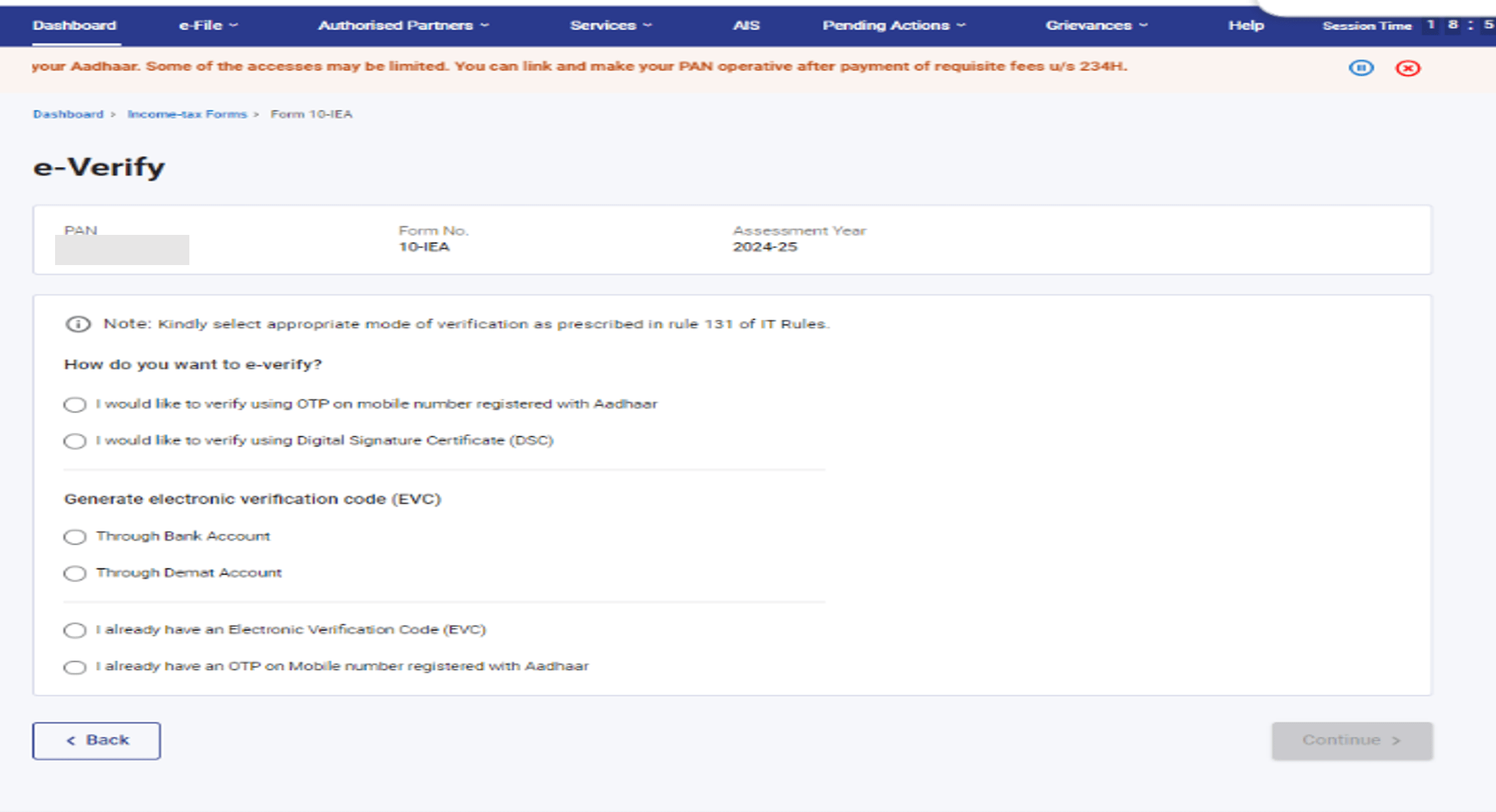

Step 10: Declaration and verification

Step 11: E-verify using Aadhaar OTP / Net Banking / EVC

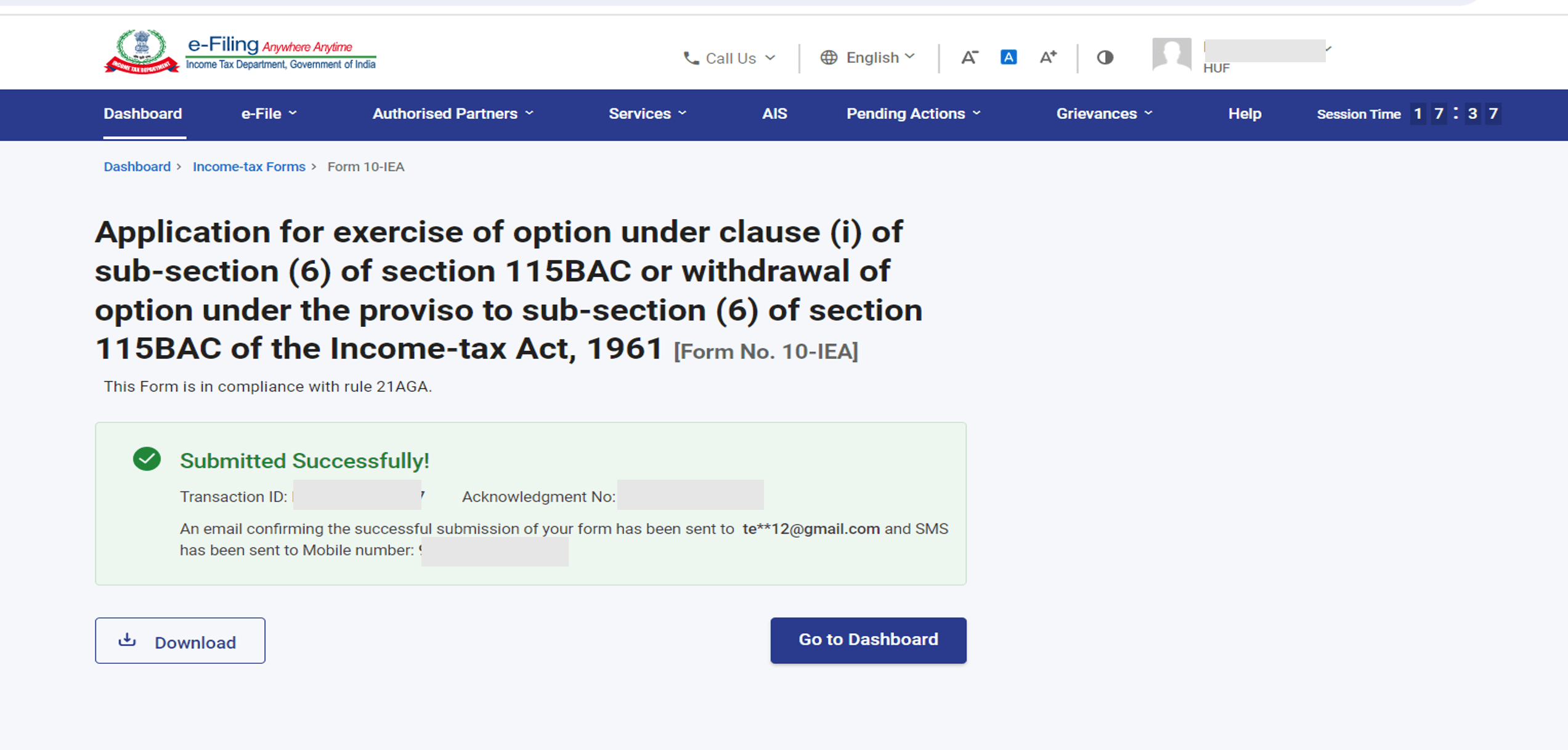

Step 12: Submit. Note the Transaction ID for reference.

Done. You're now in old regime. What Happens If You Miss the Deadline?Scenario: You realize on August 5 that you should've filed Form 10-IEA by July 31.

Common Mistakes People Make#Mistake 1: "I'll decide while filing ITR" Wrong. If you have business income, Form 10-IEA must be filed separately before ITR deadline. #Mistake 2: "I filed last year's Form 10-IEA, so I'm covered" Wrong. Form 10-IEA is year-specific. File fresh every year before ITR deadline. #Mistake 3: "I can file it anytime before March 31" Wrong. Deadline is your ITR due date (usually July 31), not financial year end. #Mistake 4: "I'll switch regimes mid-year" Wrong. Once you file ITR, you're locked for that year. Can't change. 👉 Action Steps (Do This Before July 31, 2025)Step 1: Check if you need Form 10-IEA Step 2: Calculate which regime saves you more Step 3: If old regime is better, file Form 10-IEA NOW Step 4: Set annual reminder If this saved you from a costly mistake, forward it to one friend with business/consulting/freelance income. They likely don't know about Form 10-IEA either. Got questions about old vs new regime for your specific case? Hit reply with your income details and I'll help you calculate. The fastest way to save tax isn't complicated planning. It's filing the right forms before the deadline. Connect with me on LinkedIn, I write every day to help you make smarter money decisions👇 |

Ritesh Sabharwal

Ritesh Sabharwal CFP® W.M.W #55: Do you know - Your EPF Account Has ₹7 Lakh Life Insurance? Reading time: 5 minutes - July 4, 2026 ↓ Hey Reader Have you heard about EDLI - Employees' Deposit Linked Insurance? Most people reading this right now have this benefit and are not aware. Most haven't told their families about it. Your EPF account comes with ₹7 lakh life insurance. You're paying ₹0 for it and your employer covers the premium.It sits quietly inside your EPF account. It activates...

Ritesh Sabharwal CFP® W.M.W #54: Which is better: 70-20-10 vs 50-30-20? Reading time: 5 minutes - June 27, 2026 ↓ Hey Reader One of the defining financial challenges for Indian households in 2026 is not a lack of income, but a lack of financial visibility and control. Rising living expenses, combined with unprecedented access to consumer credit through EMIs, BNPL platforms, and credit cards, have normalized spending patterns that often outpace financial priorities. Millions of Indians follow...

Ritesh Sabharwal CFP® W.M.W #53: Decode the Home Affordability Formula (3 / 20 / 30 / 40) Reading time: 5 minutes - June 20, 2026 ↓ Hey Reader Reserve Bank of India data shows housing dominates borrowing in India like no other category.Half of India's loans go to one thing: Homes. Home loans: 49%, Everything else combined: 51%. And yet, most Indians are clueless to determine if they can truly afford what they're buying. They walk into a bank. Get told they're "eligible" for X amount of loan....